Introduction

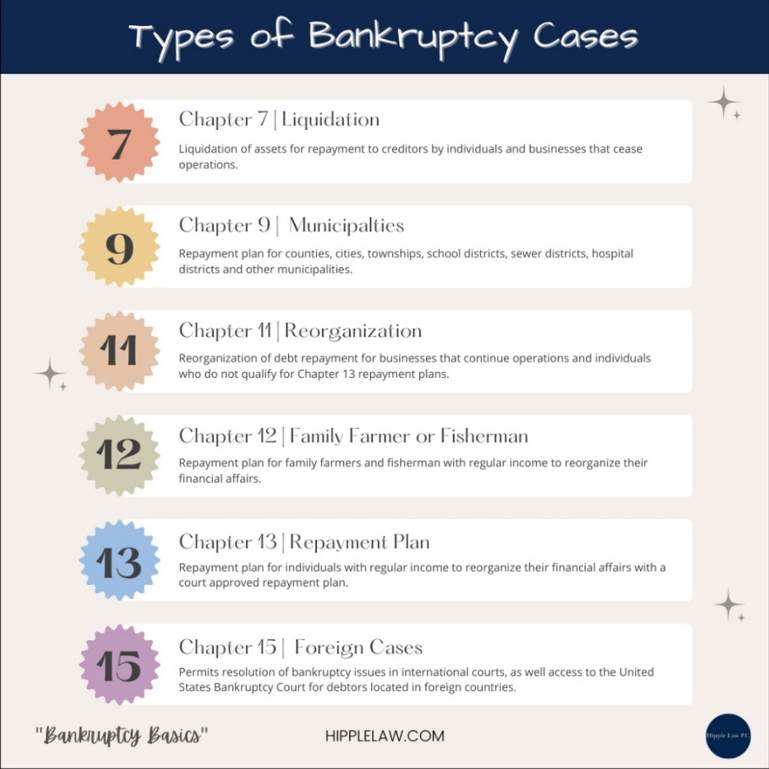

Filing for federal bankruptcy protection is not a “one size fits all” approach. Instead, federal bankruptcy law has specific “chapters” tailored for different individuals and entities that may need to file for bankruptcy protection. Title 11 of the United States Code is where federal bankruptcy law provisions can be found. Within Title 11, there are six defined chapters that contain the rules and procedures for different situations. The chapters are identified as follows: Chapter 7 (Liquidation), Chapter 9 (Municipalities), Chapter 11 (Reorganization), Chapter 12 (Family Farmer or Fisherman), Chapter 13 (Repayment Plan) and Chapter 15 (Foreign Cases).

In this post, we will review the similarities and differences between the six bankruptcy chapters.

What is Chapter 7 Bankruptcy?

Chapter 7 bankruptcy is defined as a liquidation case. In a Chapter 7 case, non-exempt assets are liquidated with repayment to creditors. A Chapter 7 case is filed for debtors in two types of situations.

The first type of Chapter 7 debtors are individuals who may need to avoid repayment of unsecured debt. In an individual case, a debtor will seek a court ordered “discharge,” where the debtor will have no liability to pay discharged debts. If necessary, an individual debtor can also choose to surrender collateral for secured debts or reject leases. It is also important to understand that the right to a discharge is not absolute. There are specific debts, such as student loans, income taxes, and domestic support, which are not dischargeable in bankruptcy.

The second type of Chapter 7 debtors are partnerships, corporations, or other business entities (non-individual) that have or want to cease operations where assets are liquidated with the proceeds used to pay creditors. A discharge is not available in non-individual cases.

The mechanics behind a Chapter 7 case allow a trustee to identify, investigate and liquidate a debtor’s non-exempt assets where the funds are used to pay allowable unsecured creditors and costs to administer the bankruptcy estate. Any secured debts or liens on property will remain valid unless there is sufficient reason for the court to approve lien avoidance. In all cases, the trustee investigates and determines whether a case has assets to pursue for turnover, which is reported to the court. Debtors are allowed to retain exempt assets, according to exemption values set by the Bankruptcy Code in each jurisdiction. In most Chapter 7 cases, a trustee will make a no asset finding without turnover, because there is little or no non-exempt equity available in assets. However, every case is different, and debtors should not assume that all of their assets are protected from turnover. Debtors are often unaware of facts in their case which could result in loss of an asset. In situations where assets are at risk, it may be prudent to file a Chapter 13 case so that a debtor can protect assets from turnover. It is also important to understand that turnover determinations are often subjective and vary by trustee.

A discharge in a Chapter 7 bankruptcy case is not guaranteed. There are pre-filing eligibility requirements, which include 1) no presumption of abuse based on a “means test” analysis of current monthly income available to pay creditors, 2) completion of a court-required credit counseling course, 3) no filing restrictions related to a filing or dismissal of a prior Chapter 7 case.

What is Chapter 9 Bankruptcy?

Chapter 9 Bankruptcy provides financially distressed municipalities protection from creditors while a plan to adjust debts is developed, negotiated, and approved. Chapter 9 applies only to entities, as defined by the Bankruptcy Code, such as counties, cities, townships, school districts, sewer districts, hospital districts and other municipalities. The Chapter 9 eligibility provisions and protections are tailored to accommodate the unique nature of municipalities.

What is Chapter 11 Bankruptcy?

Chapter 11 Bankruptcy is often referred to as reorganization. This type of case is filed by partnerships, corporations, and other business entities (non-individuals) that need reorganization to continue operations, and individuals with high debt, who do not qualify for Chapter 13 repayment plans.

In a Chapter 11 bankruptcy case for a non-individual, the debtor usually remains “in possession” to operate a business without a required trustee. In those situations, the debtor must seek court approval for business operations, as well as provide monthly budgets and a feasible plan approved by creditors. In an individual Chapter 11 case, it is not unusual for the same requirements to exist as are required for individual debtors who file a Chapter 13 case.

Any size business can file for Chapter 11 reorganization. Therefore, there are Chapter 11 provisions for small businesses intended to streamline the process and reduce costs. During February 2020, new provisions for a Chapter 11 Sub-Chapter V became effective which made the process for small businesses even more streamlined than a regular small business Chapter 11 case. A Chapter 11 case is usually expensive, complicated, and time-consuming. It is not unusual for the court to have a local rule that a Chapter 11 case cannot be filed without an attorney, and counsel for the debtor must have a co-counsel mentor or proven experience handling Chapter 11 cases in order to file a case.

What is Chapter 12 Bankruptcy?

Chapter 12 Bankruptcy is a voluntary case for family farmers and fishermen. This type of case applies to financially distressed “family farmers” or “family fishermen” with regular “annual income” to help reorganize financial affairs for payment of all or a portion of their debts with a court-approved plan. A Chapter 12 case is similar to a Chapter 13 case, although the provisions are specifically tailored to eliminate barriers with other chapters and meet the economic realities and seasonal nature of family farming or fishing businesses. A Chapter 12 case applies to two categories of debtors, namely an individual (and spouse) or a corporation or partnership (non-individual), with specific eligibility requirements for each type of case identified in the Bankruptcy Code.

In a Chapter 12 case, possession of secured property can be maintained by the debtor as long as regular payments are paid and there is trustee approval to incur any significant debt. A discharge will be granted in a successfully completed Chapter 12 case, provided certain conditions set forth in the Bankruptcy Code are satisfied. Similar to Chapter 13 cases, there are specific debts listed in the Bankruptcy Code which are not dischargeable in a Chapter 12 case.

What is Chapter 13 Bankruptcy?

Chapter 13 Bankruptcy is often referred to as the wage earner’s plan. This type of case permits a repayment plan for individuals (single and married) with regular income to reorganize their financial affairs, for all or partial payment of debts during a three- or five-year period with a court-approved plan. In this type of case, a debtor remits a monthly payment to the trustee, who administers the bankruptcy estate by sending payments to allowable creditors. During the case, creditors are not permitted to pursue any collection efforts against the debtor or any co-debtors.

Chapter 13 cases have several advantages, including 1) adjustment of timing for repayment of debts (not including mortgages), 2) ability to catch up on past-due mortgage payments to save a home from foreclosure, 3) protection of third party co-debtors from collection activities during the case, 4) dischargeability of all or a portion of certain types of debts not permitted in a Chapter 7 case, such as debts incurred to pay nondischargeable tax obligations, and debts arising from divorce property settlements, and 5) a repayment plan for sole proprietorships and unincorporated businesses without the necessity of filing a Chapter 11 reorganization case. One of the main advantages with filing Chapter 13 is treatment of the “liquidation factor” by the trustee. The liquidation factor is a calculation of the non-exempt equity that would be available to pay creditors in a Chapter 7 case from non-exempt assets. In a Chapter 13 case, the trustee does not seek turnover of assets, which could happen in a Chapter 7 case. Rather, the trustee requires an adjustment to the Chapter 13 plan payment of at least the same amount that could be obtained in a Chapter 7 liquidation case. The Chapter 13 advantage is that you can keep non-exempt assets by agreeing to pay a higher plan payment, instead of required turnover of assets to a trustee.

The main eligibility question for filing a Chapter 13 case is whether the debts in the bankruptcy estate are less than published debt limits, which are adjusted every three years to reflect changes in the consumer price index. Currently, the debt limits are total unsecured debts less than $394,725 and total secured debts less than $1,184,200. The next debt limit change is scheduled for April 1, 2022.

In a Chapter 13 case, there are specific types of non-dischargeable debts which must be repaid in full, such as domestic support, mortgage arrearages, and unpaid taxes. Otherwise, a Chapter 13 debtor can obtain a discharge from payment of a portion or all debts, provided all requirements for the case are successfully completed. There are also certain types of debts defined in the Bankruptcy Code that are not dischargeable in a Chapter 13 case, including student loans and government fines and penalties. Similar to Chapter 7 cases, there are also specific eligibility limitations for a Chapter 13 discharge, based on specific time limits related to a prior bankruptcy case dismissal or a successfully completed case.

What is Chapter 15 Bankruptcy?

Chapter 15 Bankruptcy is often referred to as “Foreign Cases”, although this chapter is technically identified as “Ancillary and Other Cross-Border Cases” in the Bankruptcy Code.

The purpose of a Chapter 15 proceeding is to be the principal door for international cooperation and communication across borders to resolve bankruptcy issues. A Chapter 15 case is appropriate when 1) a debtor who resides in another country needs to file a Chapter 7 or Chapter 11 case because the majority of assets are located in the United States, and 2) court authorization for a trustee or other entity is necessary to intervene and act in a foreign country on behalf of the bankruptcy estate. Chapter 15 cases also allow foreign creditors the right to participate in United States bankruptcy cases.

Why are Different Bankruptcy Chapters Important?

Thousands of bankruptcy cases are filed every year for individuals and businesses suffering a financial hardship. A bankruptcy case requires disclosure of all assets, liabilities, income, and expenses for individuals (and spouses), partnerships, corporations, and other business entities (non-individuals). Every debtor, whether an individual or non-individual has different financial facts that apply to their situation. The administration of a bankruptcy case is not a “one-size fits all.” Title 11 of the United States Code is organized by chapter with rules tailored to specific types of debtor situations who need federal bankruptcy protection.

Bankruptcy Chapters: Manage Financial Hardships

If you are suffering a financial hardship either individually or with your business, federal bankruptcy protection is an option for a “fresh start.” There are advantages with filing for bankruptcy to stay creditor collection activities while you eliminate a portion or all of your debt either with liquidation, repayment, or reorganization. Federal bankruptcy laws are established with different chapters so that debtors can find the best fit for their situation.

It is important to have an experienced bankruptcy attorney manage your case if you want to optimize the bankruptcy rules and protections available for your situation. Bankruptcy is more than just a list of rules. There are definitely differences with how trustees and judges oversee cases in different jurisdictions. A debtor without an attorney can be significantly disadvantaged when filing a case. A bankruptcy attorney will know the how and why to apply bankruptcy rules for a specific jurisdiction, to help protect a debtor and their property.

Contact us today to schedule a video, phone, or office consultation with an attorney to see if bankruptcy is a good option for you, and to understand how the process applies to your situation.

We use an easy online questionnaire for clients to submit their financial information and upload documents to prepare a case. You can sign-up for a FREE NO OBLIGATION PREVIEW of the online tool to see if it is a good fit for you while you explore your options. https://www.hipplelaw.com/bankruptcy/mycaseinfo/